Why 90% of Your Cash Isn't Cash at All.

An Simple Look at the USD and GBP Monetary Systems

Have you ever stopped to think about where money actually comes from? If you’re like most people, you probably picture a government printing press churning out stacks of notes. The reality, confirmed by central banks like the U.S. Federal Reserve and the Bank of England, is far more complex, fascinating—and unsettling.

The money in your bank account, the money that fuels global commerce, is fundamentally different from the coins in your pocket. This article provides a comprehensive analysis of the debt-based foundation of the modern U.S. Dollar (USD) and Great British Pound (GBP), comparing the mechanics of their respective financial systems.

1. The Foundational "Why": Money, Debt, and Trust.

Both the USD and GBP are based on the fiat monetary system, meaning their value is not backed by gold or silver, but by government decree and the public's confidence. Crucially, the system is engineered so that virtually all money is created as a liability (debt) on a bank's ledger.

A. Money as a Balance Sheet Liability (I.O.U.)

The core principle is that money is an asset for the holder but a liability for the institution that issues it.

- Central Bank Debt (Physical Cash): A Federal Reserve Note (USD) or a Bank of England Note (GBP) is a legal liability of its respective central bank. The "promise to pay" inscribed on these notes signifies this debt obligation.

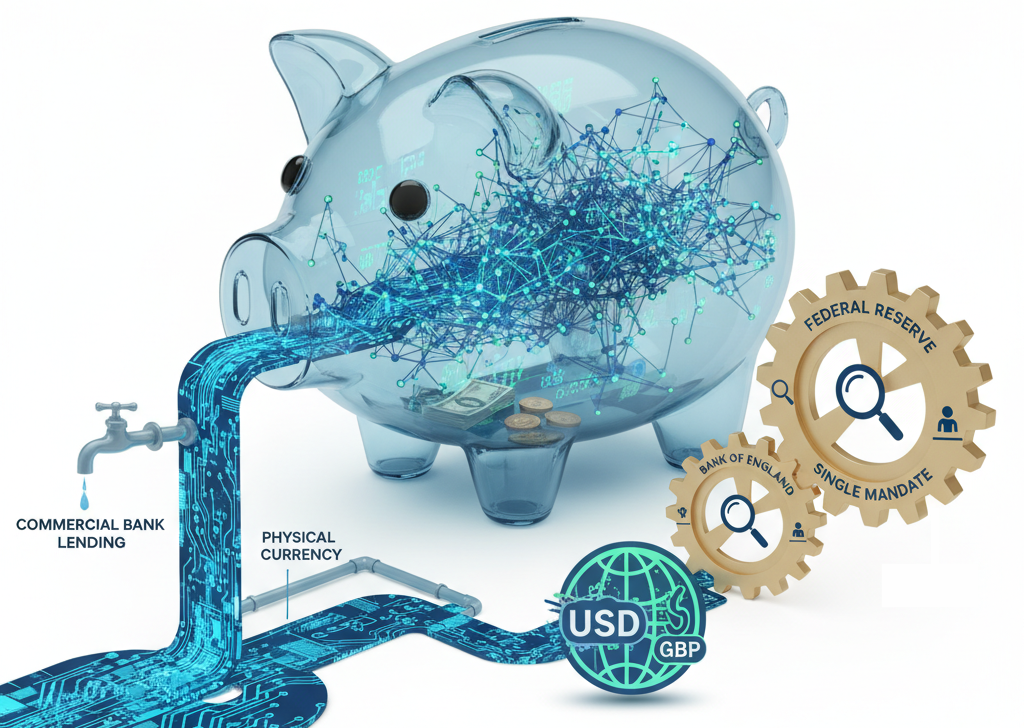

- Commercial Bank Debt (Electronic Deposits): The money you see in your checking account is a liability of your commercial bank. The bank legally owes you that balance. When money moves electronically, the bank simply transfers this liability from one customer’s account to another’s.

B. The Engine of Creation: Commercial Bank Lending

The vast majority of the money supply is created not by governments, but by commercial banks through the act of lending—a mechanism that binds the money supply directly to debt:

- The Loan Approval: A commercial bank approves a loan (e.g., a mortgage or business loan).

- Creation Ex Nihilo: The bank does not transfer existing funds. Instead, it electronically creates a new deposit in the borrower's account. This simultaneous act generates a new bank asset (the loan/debt owed by the customer) and a new bank liability (the deposit, which instantly becomes new money in the economy).

- The Result: The money supply grows when the rate of new loan creation exceeds the rate of loan repayment (which destroys money). This structure makes a growing economy dependent on continuously increasing levels of debt.

2. The "What": The Shocking Composition of the Money Supply

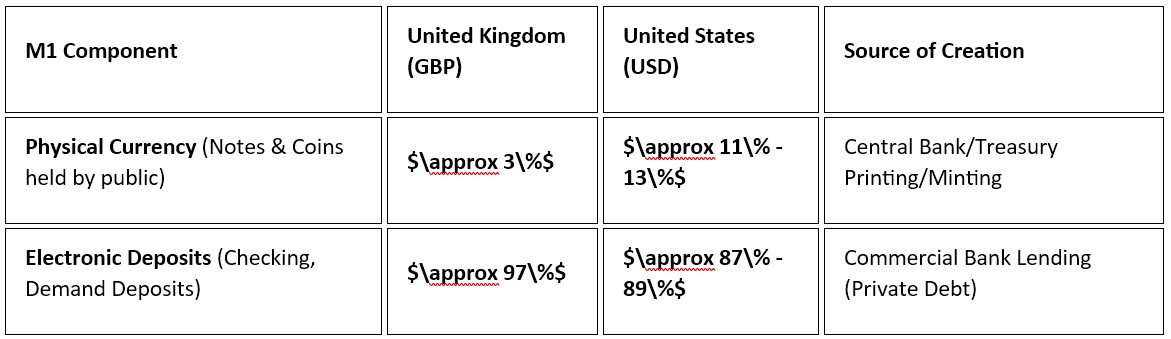

The most liquid money available for immediate spending is measured by M1 (Narrow Money). Data from both central banks confirm that physical currency is an almost negligible component of the funds we actually use.

Contextualizing the Difference

The disparity in these percentages is telling:

- The Pound's Digitization: The Bank of England explicitly confirms that only $\approx 3\%$ of the money held by individuals and companies is physical cash. The UK's highly concentrated commercial banking system and early adoption of electronic payment systems contributed to this swift transition.

- The Dollar's Global Role: The higher percentage of physical cash for the USD (up to four times the GBP proportion) is mainly due to the dollar’s status as the primary global reserve currency. Large amounts of physical U.S. dollars are held and used outside the American banking system by foreign entities, which still counts towards the U.S. money supply aggregate.

In essence, every major transaction—from salary payments to corporate spending—is conducted using electronic bank deposits, confirming that the digital balance is the dominant form of modern money.

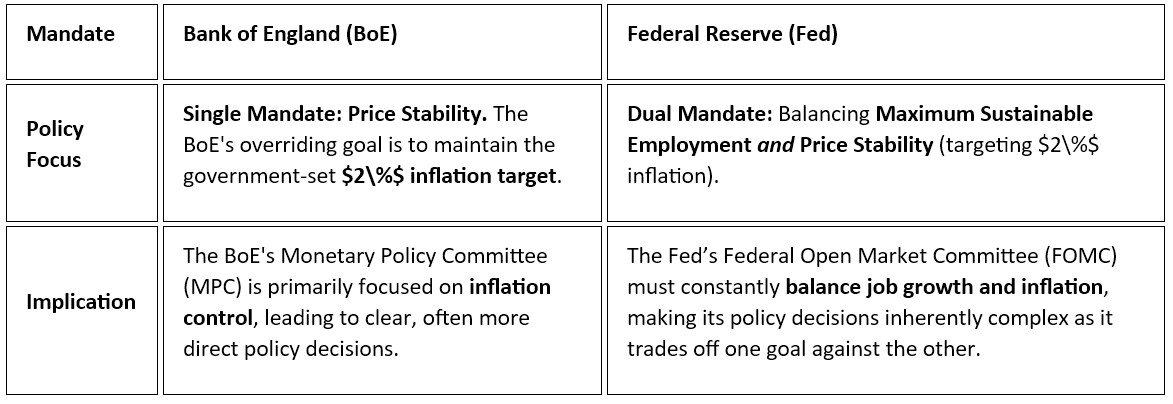

3. The "How": Central Bank Structures and Policy Mandates.️

The institutions that manage these currencies, the Federal Reserve (Fed) and the Bank of England (BoE), operate with distinct legal frameworks, influencing how they manage the money supply.

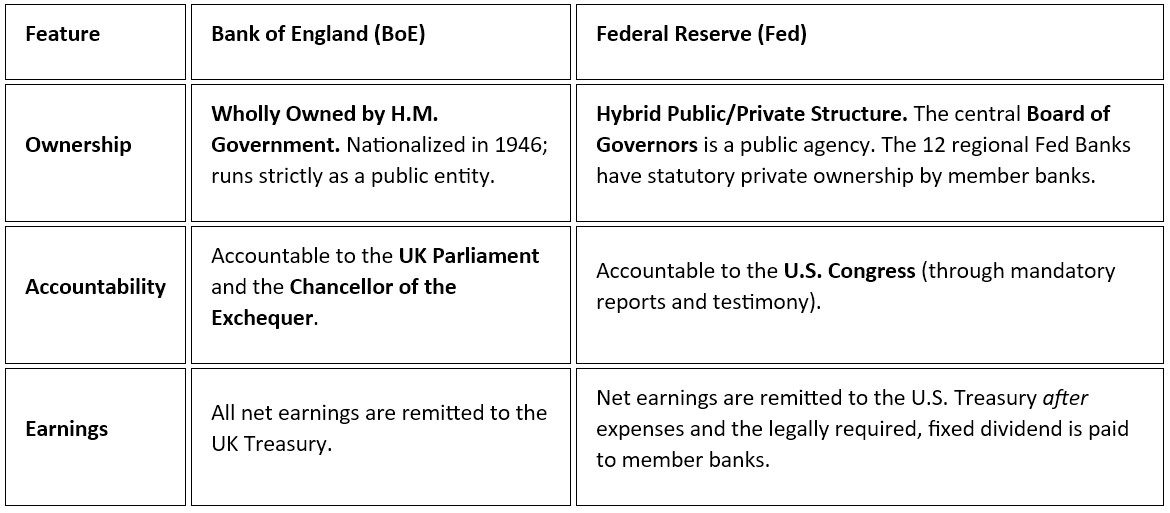

A. Institutional Structure and Ownership

B. Central Bank Independence and Policy Mandates

Both central banks maintain operational independence from the executive government, allowing them to make monetary policy decisions free from short-term political pressure. However, their primary directives differ significantly:

C. The Role of Quantitative Easing (QE)

When necessary, both central banks employ Quantitative Easing (QE)—the large-scale purchase of financial assets, typically government bonds—to inject liquidity into the financial system.

- The Purpose: QE is a mechanism for the central bank to create new electronic central bank reserves for commercial banks. This is done to lower long-term interest rates and ease borrowing conditions, stimulating the economy when short-term rates are already near zero.

- Crucial Caveat: QE does not directly transfer cash to the public; it operates within the interbank market, hoping to encourage commercial banks to increase their own lending, thereby creating more money (deposits) for the wider economy.

4. Historical and Systemic Differences

The evolution of commercial banking and deposit insurance also sets the two systems apart:

- Banking Structure: The U.K. developed a system of large, centralized nationwide branch banking over centuries. In contrast, the U.S. historically had a fragmented system of thousands of smaller, localized banks due to restrictive state and federal laws (though consolidation has occurred in recent decades).

- Deposit Protection: Both nations have robust systems to protect citizens’ electronic deposits. The U.S. uses the Federal Deposit Insurance Corporation (FDIC), while the U.K. uses the Financial Services Compensation Scheme (FSCS), guaranteeing deposits up to a specific limit.

Final Conclusion

The modern USD and GBP systems, though managed by structurally different central banks, share the same fundamental truth: the majority of money is a liability created through credit and debt. The electronic balance you see in your account is not backed by gold or physical cash, but by the ongoing stability of a system that relies on continuous credit creation to sustain economic activity. Understanding this debt-based reality is the key to understanding who controls the flow of money and the true anatomy of a modern economy.